Page 21 - 2516_ISLA_Market_Report_-_Sep_2025_v6

P. 21

20 21

Securities Lending Market Report | H1 2025

Equities

>>> APAC Equities

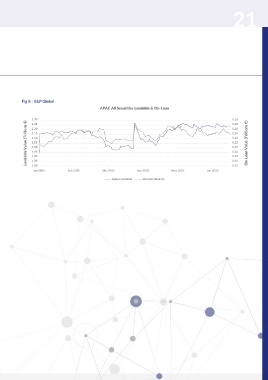

Geopolitics, coupled with regulatory changes, have been the consistent theme for the first half of the year as regulators Fig 8 - S&P Global

scrambled to implement measures to reduce the impact of geopolitical instability. Despite the volatility, major developed APAC All Securities Lendable & On-Loan

equity market indices in the APAC region, namely Japan, Hong Kong, and Australia, have outperformed the S&P500.

Part of this is due to China largely circumventing tariffs by South Korea lifted its short-sell ban on March 31 but 2.30 0.26

using other APAC countries as intermediate trading partners, implemented a new 90-day term rule on all securities 2.25 0.25

which has helped dissipate some of the geopolitical lending trades, with a maximum term of 12 months. Overall, 2.20 0.25

tensions. Chinese exports to these countries have increased Taiwan and Korea have benefited from this deregulation, 2.15 0.24

approximately 20% from January, in line with the increase with lendable balances climbing up 29% and 22% to 2.10 0.24

0.23

2.05

of US imports from these same countries. However, there $191bn and $279bn, respectively, recovering from their Lendable Value (Trillions €) 2.00 0.23 On-Loan Value (Trillions €)

has been divergence within the region, with the TAIEX, JCI, lows in March. 1.95 0.22

and KLCI exhibiting declines YTD (year-to-date). The global Deal activity in Asia has more than doubled to $650bn, 1.90 0.22

economic tension caused market-wide selloffs in April, with Japan leading the way at USD232 billion. The strong 1.85 0.21

with Singapore, Malaysia, and Australia hitting lows for the performance in Japan has been due to the buybacks of 1.80 0.21

period. However, utilization in APAC remained stable at Toyota Industries (6201 JP) in a privatization bid worth Jan 2025 Feb 2025 Mar 2025 Apr 2025 May 2025 Jun 2025

approximately 11%. Group Lendable On-Loan Balance

$34bn and Nippon Telegraph and Telephone’s (9432 JP)

In the regulatory space, the Stock Exchange of Thailand takeover of NTT Data Group (9613 JP) in an AI play worth

(SET) announced a short-selling ban from April 8 to April $16.5bn.

11, with a resumption on April 16. Furthermore, stricter Hong Kong saw healthy IPO activity, most notably with

measures restricting short-sell eligible names to the SET100 CATL (3750 HK), a Chinese EV and battery manufacturer,

are being considered. The market did not react significantly which had a $4.6bn capital raise with significant interest

to this due to the short duration of the ban, and on-loan from the borrower community. CATL continues to be well

balances remained largely stable.

utilized at nearly 95% and borrow levels of 16%. Sector-

In Taiwan, temporary market stabilization measures were wise, there is continued interest in the real estate sector,

introduced on April 7, reducing the daily short-sell quota with Vanke (2202 HK) remaining at the top of short-interest

from 30% to 3% and increasing the margin requirement lists globally, commanding borrow fees of 2%. Technology

for OTC securities from 90% to 130%. The industrials and continues to be an area of demand, with Alibaba Health

electronics sectors continue to be in demand, with notable (241 HK) remaining highly utilized at a 6% volume-weighted

names including PCL Technologies (4977 TT), Gudeng average fee.

Precision (3680 TT), and New Era Electronics (4909 TT)

trading at special rates of 7% to 12% for the period.